Find every pension you've earned, across every country

Tell us where you've worked and PensionChart shows what you're likely owed, how your pensions affect each other, and the deadlines you can't miss.

Free to start — just your email, no card.

Full picture €99, once · 47 countries · no account-linking · 30-day money-back

Pensions are designed for people who never leave home

You've built a career across borders. But your pension entitlements are scattered across countries, buried in disconnected government portals, with rules no single financial advisor fully understands. You're left choosing between expensive country-by-country financial advice, hours of DIY research across fragmented government websites, or simply hoping it'll sort itself out closer to retirement. Until now, there's been no solution for the one thing you actually need: a clear, consolidated view of everything you've earned, in one place, on one timeline. That's PensionChart.

It's not just each pension, it's how they interact

Most tools value each pension on its own. PensionChart looks at your exact combination of countries and flags where one can change another's tax, eligibility, withdrawal access, or claim timing — plus currency exposure across your retirement income.

Everything you need to manage global pensions

Purpose-built for people who have worked across borders.

How it works

Get your complete pension picture in three simple steps.

Add your countries

Tell us where you've lived and worked

See your likely pensions & deadlines

The free Finder teaser shows what you're probably owed — before you pay anything

Unlock your full Action Plan

Who to contact, exactly what to ask, and what to include — for every country

Likely entitlement · state

🇬🇧 New State Pension

Who to contact

Check Your State Pension Forecast · official portal ↗

What to ask

“Do you hold a pension or contribution record for me under New State Pension — including any previous scheme names — for my time there (1989–2001)?”

What to include

- Your full name (and any previous names)

- The dates you lived and worked there (1989–2001)

- Your date of birth

- Employer names during that period

One of the ~22 cards in a typical 3-country Action Plan — who to contact, exactly what to ask, and what to include. Unlocked once, yours forever.

Sound familiar?

PensionChart is built for careers like yours.

Four countries. Four pension pots. No idea what any of them are actually worth. He's been meaning to sort it out for years but never knows where to start. There's no single place to see everything, so it stays on the "someday" list.

🇬🇧 British Sales Executive

Every financial advisor he's worked with has been brilliant within their own country and completely lost outside it. Nobody has the full picture. He walks into meetings knowing more about his cross-border situation than the person he's paying for advice.

🇨🇦 Canadian Management Consultant

Five years in the Gulf. No pension to show for it, just an end-of-service gratuity she spent long ago. She didn't realise until much later that those were "dark years" for retirement savings, and now she's trying to figure out how to close the gap.

🇦🇺 Australian Senior Project Manager

The EU is supposed to make cross-border pensions seamless. In practice, tracking contributions across three national systems is anything but. Her accountant handles taxes fine. The pension side? Nobody owns it.

🇫🇷 French UX Designer

Four countries. Four pension pots. No idea what any of them are actually worth. He's been meaning to sort it out for years but never knows where to start. There's no single place to see everything, so it stays on the "someday" list.

🇬🇧 British Sales Executive

Every financial advisor he's worked with has been brilliant within their own country and completely lost outside it. Nobody has the full picture. He walks into meetings knowing more about his cross-border situation than the person he's paying for advice.

🇨🇦 Canadian Management Consultant

Five years in the Gulf. No pension to show for it, just an end-of-service gratuity she spent long ago. She didn't realise until much later that those were "dark years" for retirement savings, and now she's trying to figure out how to close the gap.

🇦🇺 Australian Senior Project Manager

The EU is supposed to make cross-border pensions seamless. In practice, tracking contributions across three national systems is anything but. Her accountant handles taxes fine. The pension side? Nobody owns it.

🇫🇷 French UX Designer

Three countries. Three pension systems. Three government portals in three languages. She logs into each one separately, tries to compare numbers in different currencies, and closes her laptop no wiser than before.

🇳🇱 Dutch Marketing Director

She doesn't need another government website. What she needs is to see the timeline. Her UK pension starts at 67, her US Social Security at 70, and there's a three-year gap nobody warned her about. That single insight changes everything about how she plans the next decade.

🇮🇳 Indian Software Engineer

Retired now. Wishes he'd seen the full picture ten years earlier.

🇨🇭 Swiss Operations Director

She assumed her foreign pensions weren't worth chasing from overseas. She was wrong, but it took seeing everything consolidated in one place to realize what she was leaving on the table.

🇧🇷 Brazilian HR Executive

Three countries. Three pension systems. Three government portals in three languages. She logs into each one separately, tries to compare numbers in different currencies, and closes her laptop no wiser than before.

🇳🇱 Dutch Marketing Director

She doesn't need another government website. What she needs is to see the timeline. Her UK pension starts at 67, her US Social Security at 70, and there's a three-year gap nobody warned her about. That single insight changes everything about how she plans the next decade.

🇮🇳 Indian Software Engineer

Retired now. Wishes he'd seen the full picture ten years earlier.

🇨🇭 Swiss Operations Director

She assumed her foreign pensions weren't worth chasing from overseas. She was wrong, but it took seeing everything consolidated in one place to realize what she was leaving on the table.

🇧🇷 Brazilian HR Executive

How PensionChart compares

A country-by-country advisor, DIY portal-hopping, or one consolidated picture.

| Country-by-country advisor | DIY portal-hopping | PensionChart | |

|---|---|---|---|

| Cost | Per-country fees, every year | Free — except your evenings | €99 once, every country included |

| Cross-border rules | Expert in one country, lost across borders | You reconcile the rules yourself | 47-country directory + treaty rules |

| How pensions interact | Each pension valued on its own | No combination view | Combination alerts — tax, timing, eligibility |

| Deadlines | You track them yourself | Easy to miss | On your timeline, flagged before they close |

| Account access | Often wants full financial disclosure | A login for every portal, in every language | No account-linking, ever |

| Your picture | Locked in PDF attachments | Scattered across tabs and spreadsheets | One consolidated picture — yours forever |

Built by Marco, an expat with pensions in four countries (🇨🇦 🇮🇹 🇺🇸 🇳🇱). He needed this tool and couldn't find it. Read the story →

Frequently asked questions

Everything expats need to know about managing pensions across borders.

No, this is the most common fear, and it's unfounded. In virtually every developed country, pension rights you've already earned are legally yours to keep, regardless of where you live when you retire.

Your entitlements simply stay where they were earned, continuing to be managed or invested, until you reach that country's retirement age and claim them. The Dutch AOW, the UK State Pension, US Social Security, German Rentenversicherung, Canadian CPP — all of them will pay you abroad.

The real risk isn't losing your pension. It's losing track of it. Pension providers won't chase you across borders, and contact details go stale when you move. The first step is knowing what you have and where it is — which is exactly what PensionChart helps you build.

It depends on the country, but the short answer is: those years probably count for something, even if the amount is small.

Most countries have a minimum contribution period before you qualify for any benefit, typically 5–10 years. If you fall short, some countries let you combine your work years from multiple countries using totalization agreements to meet the threshold. Others, like Germany, offer a lump-sum refund of your contributions if you worked fewer than 5 years and have permanently left — though accepting the refund permanently cancels those years from your record.

Within the EU, any work period counts toward a proportional pension from each country, even just a year or two. Outside the EU, the rules vary considerably.

The key thing is not to assume short stints are worthless without checking. Many expats are pleasantly surprised.

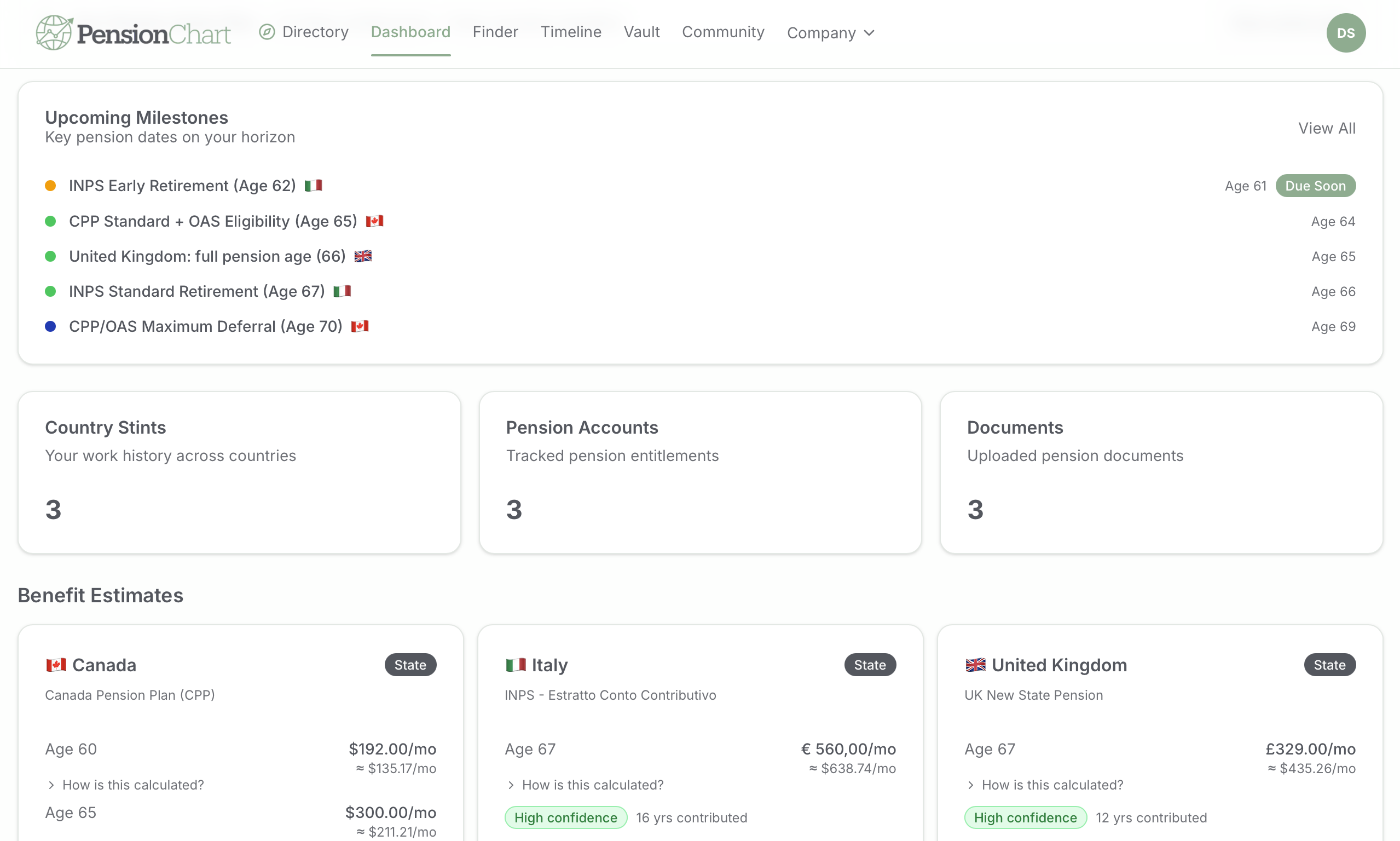

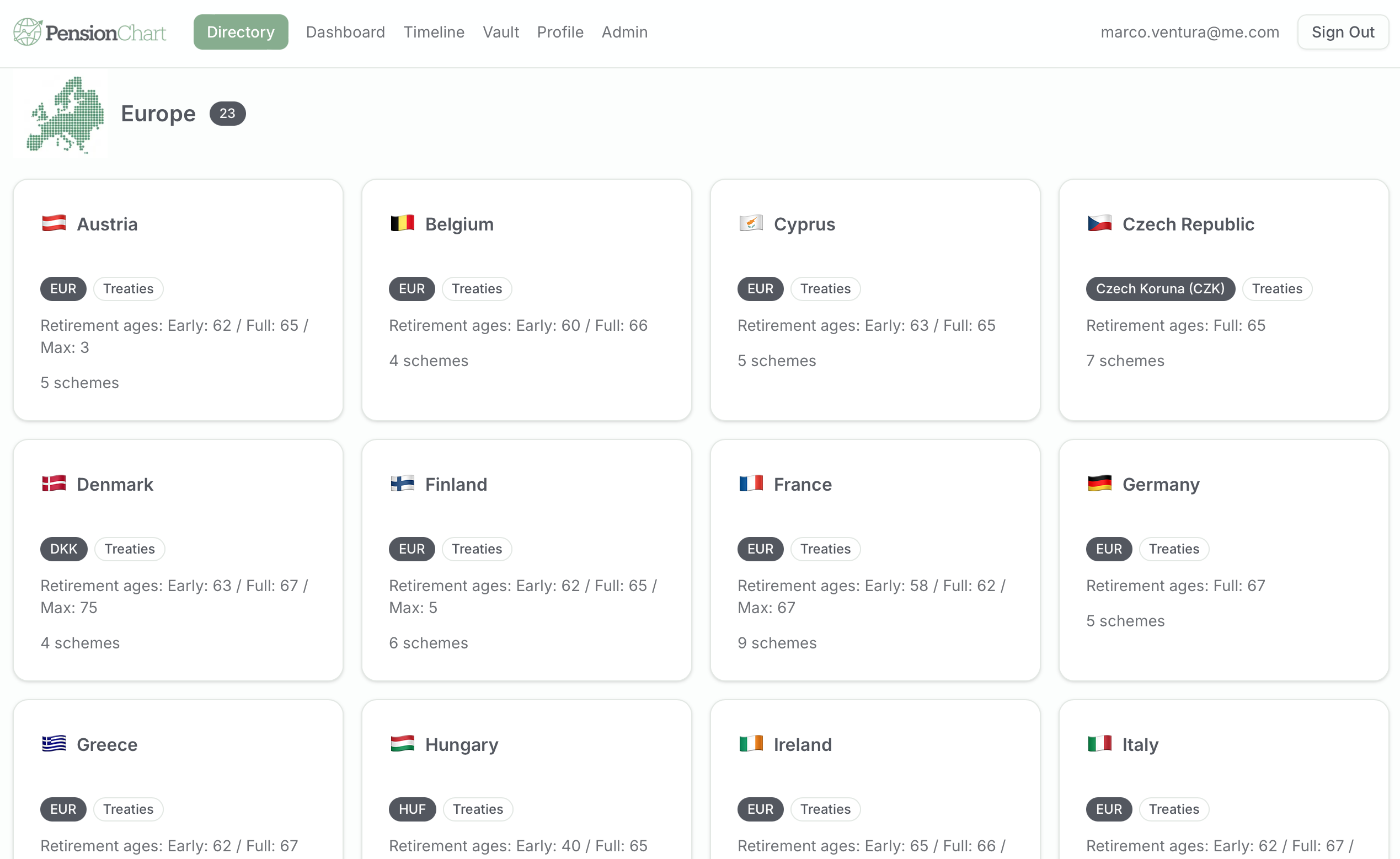

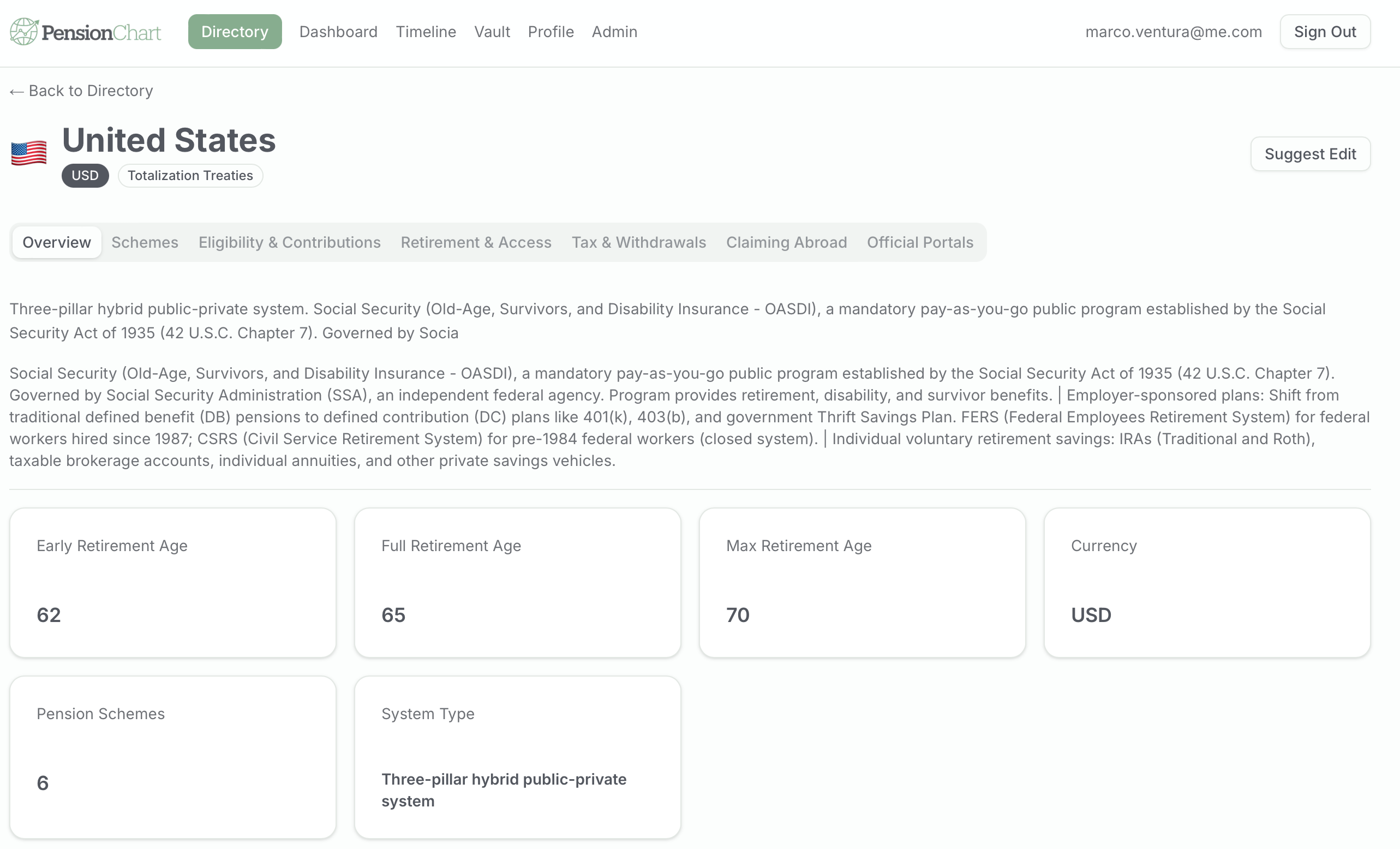

This is one of the most common practical challenges for globally mobile professionals. Every country has its own pension system, and the options today are fragmented — government portals in different languages, country-specific advisers, and spreadsheets. PensionChart brings the research and your own records together in one place. We maintain a directory covering pension systems in 47 countries, kept current by ongoing AI research, reviewed by our team before publishing, with input from our community of expat professionals. PensionChart also gives you one place to track your pension data on an interactive timeline, so you can see your full retirement picture rather than a stack of disconnected statements.

Probably not, but avoiding double taxation requires actively using the right mechanisms. It doesn't happen automatically.

Most countries have tax treaties that allocate the right to tax pension income. The general principle is that your pension is taxed where you live, not where you earned it. In practice, this means you can usually apply for an exemption from tax being withheld at source in the paying country, so you only pay tax in your country of residence.

The complication for US citizens is that the US taxes based on citizenship, not residency. Even with a tax treaty in place, the US can still tax your foreign pension income. The mechanism that prevents actual double taxation is the Foreign Tax Credit, not the Foreign Earned Income Exclusion, which only applies to earned income, not pensions.

The practical takeaway: double taxation is preventable, but you need to be well informed and plan accordingly.

Sometimes, yes — and this catches many expats off guard. In some countries, employer contributions to a foreign pension plan are treated as taxable income in the year they're made, not when you eventually receive a pension. This depends entirely on whether a tax treaty recognizes the foreign plan as equivalent to a domestic one.

For US taxpayers specifically: most foreign pension plans are not "qualified" under US tax law. Unless a treaty specifically provides tax deferral, as the US–UK treaty does, and the US–Canada treaty does for RRSPs, the IRS may treat employer contributions as current taxable income. This is one of the most common and costly surprises for American expats.

If you're currently working abroad and contributing to a local pension, it's worth confirming how it's treated in your home country before the tax bill arrives.

Almost certainly yes, and the consequences of not doing so can be severe.

For US citizens and residents, foreign financial accounts — including most individual pension accounts abroad — must be reported annually if the aggregate value exceeds $10,000 at any point during the year (FBAR, FinCEN Form 114). A separate FATCA report (Form 8938) applies at higher thresholds. Non-willful penalties start at over $12,000 per account per year. Willful non-compliance is significantly worse.

For UK residents, worldwide income including foreign pension income must be declared on your self-assessment return. Australian residents have similar obligations to the ATO.

If you've fallen behind on reporting, there are usually catch-up options — the US IRS Streamlined Filing procedures allow penalty-free corrections if the failure was non-willful. Don't assume it's too late to sort out. Act sooner rather than later.

This is one of the most underappreciated challenges of multi-country retirement — and one of the most consequential financially.

Retirement ages vary significantly across countries. The current range runs from 60 to 70 across OECD nations, with most between 65 and 67. When you've worked in three countries with pension ages of 62, 65, and 67, you face years of income gaps and sequencing decisions that don't exist for single-country retirees.

A few principles that help:

- Don't assume you have to claim everything at once. You can often take one pension earlier while deferring another for a higher amount — provided you have income to bridge the gap.

- Delaying is often rewarded. US Social Security grows by roughly 8% per year for each year you delay past full retirement age. Other countries have similar incentive structures.

- Map your income by year. Knowing when each pension starts, in which currency, and at what amount lets you identify gaps, model tax exposure, and make deliberate decisions rather than reactive ones.

PensionChart is designed to help you see this picture — all your pensions on a single timeline, so sequencing decisions become clearer.

The process is manageable, but it requires you to be proactive — no country will automatically start paying you just because you've reached retirement age.

The general process:

- Apply in advance. Most countries recommend applying 3–6 months before you reach their retirement age. The EU explicitly notes that "drawing a pension from several countries can be a long procedure."

- Contact each country's international claims unit. Most have dedicated departments for non-resident claimants. The UK's International Pension Centre and the US Social Security Administration's Office of International Programs handle these routinely.

- Have your documents ready. You'll typically need proof of identity, employment records, your foreign social security number or equivalent, and bank account details for payment.

- File in one country where possible. Under many bilateral agreements, filing in one country can initiate the claim in the other automatically.

The practical challenge is knowing when each pension age arrives for each country. Keeping a clear record of your retirement dates across countries is the kind of thing PensionChart tracks for you.

If you worked in the Gulf as an expat, you almost certainly have no access to the local state pension system, which covers only citizens. What you likely do have is an End-of-Service Gratuity (EOSG), a lump sum calculated based on your years of service and final salary, paid by your employer when you leave.

In the UAE, this is typically 21 days' basic salary per year for the first 5 years, and 30 days thereafter, capped at 2 years' total salary. It's not a pension — it's a termination payment. There's no ongoing investment, no interest, and no protection if your employer goes bankrupt.

Newer initiatives are changing this slowly. Dubai's DIFC introduced a mandatory savings scheme (DEWS) in 2020. The broader UAE is piloting voluntary savings options. But for most expats who worked in the Gulf before these schemes, there's simply no residual entitlement — everything was paid at the end.

The implication is that years spent in the Gulf are "dark years" for pension accrual unless you were actively contributing to a home-country pension voluntarily during that period, or continuing contributions to your home system.

This decision is more complex across borders than it is domestically, because each option may be taxed very differently depending on which countries are involved.

The classic example: the UK allows you to take 25% of your pension tax-free as a lump sum. But that 25% is only automatically tax-free in the UK. If you're a US resident, you need to claim the benefit under the US–UK tax treaty (by filing Form 8833), otherwise the IRS treats the full amount as ordinary income.

More broadly:

- Lump sums give you control — you can invest, currency-hedge, or use for estate planning. But large lump sums can push you into higher tax brackets in a single year.

- Regular payments provide predictability and longevity protection, but lock you into a currency and income level.

- Partial withdrawals over multiple years often offer the best of both, managing tax exposure in each country while retaining flexibility.

The right answer depends on your tax residency, which treaty provisions apply, your other income sources, and your currency situation. This is one area where specialist cross-border financial advice pays for itself.

Multi-currency pension income is both a strength and a risk. Having income in GBP, EUR, USD, and AUD provides natural diversification, but exchange rate movements can quietly erode the real value of each stream.

Some practical steps:

- Open bank accounts in each pension currency rather than converting everything immediately. Convert when rates are favorable rather than automatically.

- Match currency to spending where possible. If you retire to France, your EUR pension is naturally hedged against EUR costs. Your USD pension is an exposure.

- Consider specialist FX brokers for large regular conversions — they typically offer significantly better rates than retail banks.

- Don't project retirement income at today's exchange rates. A 15% currency shift over 5 years can have the same effect as a significant cut in pension income.

The key is making these decisions deliberately rather than letting them happen by default. Knowing the currency of each of your pensions, along with the amounts, is the starting point.

The research is consistent — the same mistakes appear on every forum and in every advisory firm's client stories:

Not reporting foreign pension accounts. FBAR and FATCA penalties are not theoretical — they're levied routinely, and they're large. If you're a US citizen with overseas pensions and you haven't been reporting them, address this now using the IRS's Streamlined Filing procedures.

Assuming your home-country pension plan is treated the same abroad. A Roth IRA is a foreign trust in some countries. An Australian super fund may be a foreign trust in the US. A UK SIPP may hold investments the IRS classifies as PFICs. The tax treatment of familiar vehicles often changes completely when you cross a border.

Taking a pension transfer without expert advice. Many expats have lost significant retirement savings by transferring UK pensions into offshore QROPS schemes that were poorly structured, heavily commission-loaded, or simply inappropriate. If anyone cold-contacts you about a pension transfer, treat it as a warning sign.

Not claiming pensions you're owed. Simply not knowing you're eligible, or not going through the administrative process of claiming, is remarkably common. Pension providers don't chase former workers across borders.

Waiting too long to get the full picture. The earlier you understand what you have across all countries, the more options you have. Many decisions — like whether to pay voluntary National Insurance contributions in the UK, or preserve versus claim a German pension refund — close permanently after a certain point.

Yes, several things have time-sensitive windows that close permanently.

UK National Insurance voluntary contributions. If you've worked in the UK and have gaps in your National Insurance record, you may be able to fill them to increase your UK State Pension. The rules changed in April 2026 — Class 2, the cheaper rate for overseas contributors, was abolished — so topping up costs more than it used to, but it can still be excellent value. The window is also narrowing: gaps older than roughly six tax years can no longer be filled, and the current top-up route tightens further on 6 April 2027. For some people that's £7,400+ of lifetime State Pension at stake. Check your NI record at gov.uk/check-state-pension and make the decision deliberately before the window closes.

Germany's refund window. If you worked in Germany for fewer than 5 years and have permanently left, you may be eligible to claim a refund of your contributions — but taking the refund cancels those years forever. The alternative is preserving them toward a future proportional pension. This decision should be made deliberately, not by default.

Keeping your contact details updated. With every pension provider in every country. Annual statements go to your address on file. If you've moved without updating them, you may be missing important communications — including the notice that your pension is about to start.

In January 2025, the Social Security Fairness Act repealed two provisions that had significantly reduced Social Security benefits for people who also received a foreign pension: the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO).

The WEP had reduced US Social Security by an average of around $360/month for people who received income from a non-covered pension, including many foreign state pensions. That reduction no longer applies. If you're currently receiving reduced Social Security because of WEP, your benefit should have been automatically increased, and you should have received a retroactive lump sum payment covering January 2024 onward.

If you previously decided not to apply for Social Security because WEP made it not worthwhile, it's worth revisiting that decision now. You may be eligible for significantly more than you assumed.

Start with an inventory, not a strategy. Before you can make any decisions, you need to know what you have. PensionChart can help you a great deal in this process. Work through each country where you've lived or worked and ask: did I contribute to any pension system there? That includes state pensions, employer pensions, and any private savings. For each one, try to identify the name of the scheme or provider and an approximate amount or years of contribution. Our Global Pension Directory can help you in conducting this research if you don't remember all the details.

That's it to start. Once you can see everything in one place — amounts, currencies, retirement ages, and projected income — the decisions about timing, tax, and currency become much more manageable. PensionChart is built specifically for this step: giving you one place to organize and track what you've built across every country, so you can see your complete retirement picture for the first time.

Pay once to see your whole pension picture

Unlock your consolidated picture forever. Keep it fresh for a little each year — or own everything for life.

No credit card required.

- Pension Finder teaser — likely pensions & deadlines

- Build your pension timeline (up to 5 countries)

- Read-only pension directory

- Expat community forum access

- Full per-country Finder action plan

- Document uploads & AI analysis

- Income projections (how much you'll receive)

- Combination alerts & downloadable report

Own your consolidated pension picture — forever.

- Pension Finder — full per-country action plan

- Every country you've worked in — one price (no per-country fees)

- Upload statements & AI document analysis

- Your full consolidated dashboard & figures

- Income projections across every country

- Cross-border combination alerts (tax, timing, eligibility)

- Advisor sharing & downloadable report

- View & re-download your picture — forever

Everything, forever — including Keep Current.

- Everything in Unlock — forever

- Keep Current included — forever

- Founding member — locked-in price

- Early access to new countries

- Priority feature requests

Pay once · no subscription · 30-day money-back guarantee — full refund any time before you export your report. Refund policy

Free global pension directory

Browse pension systems, retirement ages, and contribution requirements for 47 countries. Each country's overview is open to everyone — a free account unlocks schemes, eligibility, tax and claiming.

Every guide is researched from official sources and human-reviewed before we publish. How we verify

Take control of your international pensions

PensionChart helps globally mobile professionals see and understand their pension entitlements across every country they’ve worked in — all in one place.